Thinking about owning a home in Kuwait can bring up a lot of questions about affordability and financial planning.

The process may feel overwhelming, especially if you’re trying to balance family needs, long-term investment goals, and the realities of today’s property market.

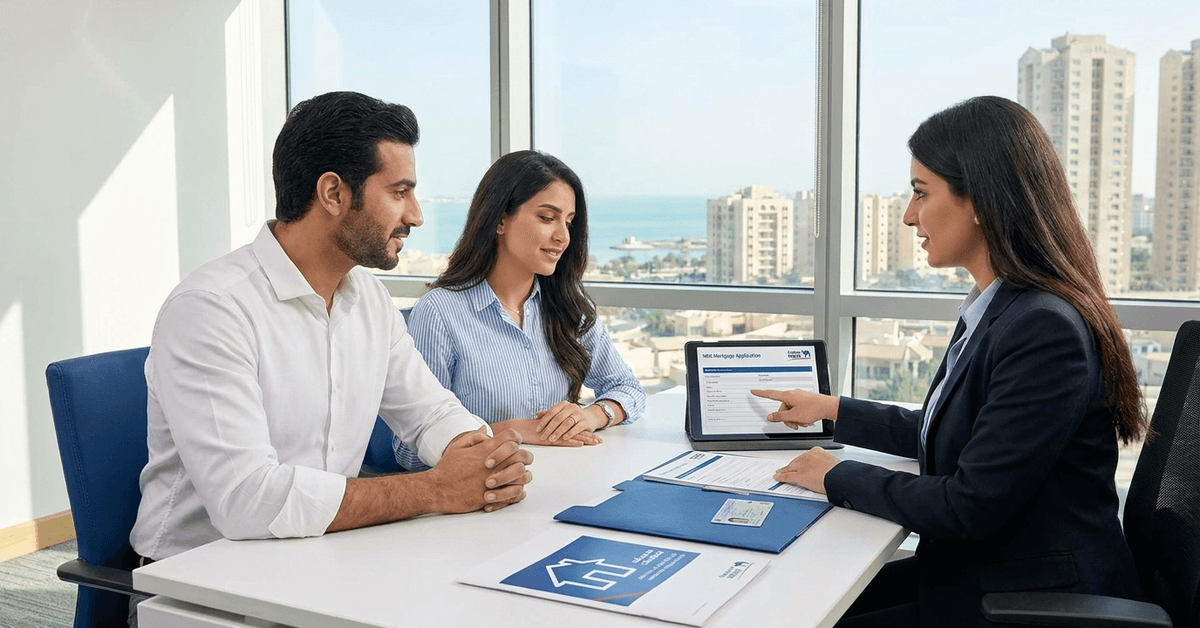

For many, the National Bank of Kuwait (NBK) mortgage program offers a pathway to homeownership that’s grounded in flexibility.

Why Choose an NBK Mortgage for Your Home Purchase?

Choosing a mortgage is never just about numbers; it comes down to trust, convenience, and honest terms.

For residents and nationals in Kuwait, NBK’s mortgage services often appeal for a few key reasons. Let’s look a little closer.

Up to 80% Home Financing

Accessing up to 80% financing for your new home can reduce the strain of collecting a huge down payment. In some ways, this can make it easier to enter the housing market, perhaps earlier than expected.

Flexible Repayment and Loan Terms

NBK’s approach seems to favor diverse needs. Mortgage terms can be adapted in both length and structure to help cater for salary levels, employment situations, and future financial changes.

Support for Kuwait Nationals and Expats

NBK provides mortgages to both Kuwaiti citizens and, with certain conditions, expatriate residents. This opens up access to a wider range of the population looking to invest in property.

Straightforward Application Process

Though any mortgage application takes effort, NBK’s process is designed for clarity and speed. Most of the paperwork and communication is streamlined and digital-first, at least in the initial stages.

Eligibility and Documentation for NBK Mortgage Loans

Understanding eligibility can clear up much of the anxiety around mortgages. NBK, like other banks, maintains a checklist to help potential borrowers assess their own suitability upfront.

Basic Eligibility Criteria

Basic eligibility requirements help determine whether you're ready to apply for an NBK mortgage. Understanding these criteria beforehand can save time, improve preparation, and make the application process much smoother.

- Applicant should be at least 21 years old.

- Salaried or self-employed with stable, verifiable income sources.

- For expats, typically a valid residency permit and proof of employment are required.

- No history of serious loan defaults or open legal cases.

Required Documents

Preparing the required documents in advance helps speed up the mortgage application process.

Having complete and accurate paperwork also reduces delays and makes it easier for the bank to assess your eligibility.

- Copy of Civil ID and proof of residence

- Salary certificate or proof of income

- Bank statements (usually last 3–6 months)

- Property title deed and valuation documents

- Employment contract or trade license (if self-employed)

- Valid passport (especially for expatriate applicants)

NBK Mortgage Features That Stand Out

There are so many options on the market that it’s easy to get lost in similarities. Still, a few NBK mortgage features do stand out, at least on paper, and may tip the balance for some buyers.

Competitive Interest Rates

NBK is known to periodically adjust rates to stay in line with market conditions, which might help borrowers take advantage of favorable periods. There’s variation based on the loan amount, property type, and applicant profile.

Flexible Payment Options

Borrowers can select repayment timelines to better fit savings habits and long-term plans—within approved bank limits.

Options for partial prepayment or early settlement are also generally available, though it’s wise to check current terms for penalties or conditions.

Insurance Integration

Most NBK mortgages come bundled with property insurance, and in some instances, life insurance. This can add a layer of reassurance, even if it’s not something most homeowners like to think about right away.

Multi-Currency Support

For some expatriates, the possibility of multi-currency mortgage arrangements offers flexibility with international moves or future employment changes. This feature is not always standard and may involve specific criteria.

How NBK Mortgage Compares with Other Lenders in Kuwait

Comparing mortgage offers is always a good habit, but not everyone has time to dig into the fine print of every deal. Sometimes, merely knowing the core differences can help make the decision easier.

Maximum Financing Amounts

While 80% financing is considered generous, a few competitors may match this on occasion. However, NBK chooses to emphasize consistency and reliability in loan disbursement and after-sales support.

Special Packages and Promotions

From time to time, NBK may offer special deals for government employees, first-time buyers, or certain housing segments. These can include discounted administrative fees or favorable rate fixes for the first year or two.

Application Steps for NBK Mortgage Loans

Applying for a mortgage at NBK is a linear process but involves several phases. Even if it sometimes feels repetitive or redundant, it does aim to protect both the borrower and the lender.

- Collect all the required documentation.

- Schedule an appointment with an NBK mortgage officer (online or in-person).

- Submit application and documents for pre-approval assessment.

- Review loan quote, including rate, tenure, and eligible amount.

- Property undergoes official valuation and legal verification.

- Upon final approval, sign the agreement and commence disbursement process.

Tips for Evaluating Kuwait Mortgage Offers

Even after identifying NBK as an option, it pays to make a thorough review of the market. Sometimes, banks update their requirements or launch new digital tools, which can affect terms or even approval speed.

Don’t Ignore Hidden Fees

I’ve heard from people who felt caught off guard by administrative or insurance fees—they can be a little confusing if buried deep in the contract.

Check for Prepayment Penalties

Flexibility is great, but sometimes lenders charge fees for early repayment or partial settlements. It’s best to clarify this in advance, even if you’re unsure whether you’ll use the feature.

Local vs. International Lenders

Some buyers weigh the benefits of a familiar Kuwaiti bank against international names. Each brings different perks, but NBK’s advantages often relate to deep local experience and on-the-ground support. Still, it can’t hurt to weigh both.

Legal and Tax Considerations for NBK Mortgages

Kuwait’s laws around home loans aim to protect borrowers, yet can sometimes seem opaque to first-time buyers. As of now, gains on residential property aren’t heavily taxed, but this may change in the future.

Property Registration

After the mortgage is approved, proper property registration with Kuwaiti authorities is mandatory. The process can require additional documentation and might take several weeks to complete.

Inheritance and Succession Laws

For Kuwaiti nationals, Islamic inheritance laws may affect property succession. Expatriates should seek professional legal advice related to home loans, especially where international family interests are involved.

Frequently Asked Questions about NBK Mortgages

Potential homeowners often share similar concerns. Here are a few recurring questions, though these aren’t ‘one-size-fits-all’ and some details may shift over time.

- Is a fixed interest rate available for the entire mortgage period? Sometimes, yes—but only as a short-term promotional rate.

- Can the loan term be altered after disbursement? In certain situations, with bank approval and possibly extra fees.

- Are there mortgage options for off-plan property purchases? NBK’s policies vary; it’s best to verify current terms with a mortgage officer.

Conclusion

Choosing the National Bank of Kuwait (NBK) Mortgage can make homeownership more achievable with competitive financing, flexible repayment options, and support for different property needs.

Before applying, compare available mortgage plans, review eligibility requirements, and ensure the monthly payments fit comfortably within your long-term financial goals and budget.

Note: There are risks involved when applying for and using credit. Consult the bank’s terms and conditions page for more information.